Dr William Chung, Associate Professor in the Department of

Management Sciences, argues that access to cheaper Liquefied

Natural Gas (LNG) world markets can allow Hong Kong to

enjoy a coal-free, nuclear-free future. The key to net zero

carbon emissions by 2050 is carbon offsetting and this creates

an opportunity to green the Belt and Road.

Climate change is the

defining issue of our time

and we are at a defining

moment. The United Nations

has declared that "rapid and farreaching"

changes are required in

order to keep the global average

temperature rise below 1.5°C

relative to pre-industrial levels. A

special report released by the UN

Intergovernmental Panel on Climate

Change in October 2018 set an

urgent new goal: net zero carbon

emissions by around 20501. This

article shows how Hong Kong can

achieve this emissions target by

relying primarily on LNG, and using

carbon offsets to create a win-win

situation and green the Belt and

Road.

The Hong Kong government is

making its contribution. A public

engagement document "Longterm

Decarbonisation Strategy"

was issued through the Council for Sustainable Development of the

Environment Bureau in June 2019.

It seeks to "provide a platform to

gauge the views of the community

in formulating Hong Kong's longterm

decarbonisation strategy,

charting practical pathways and

developing feasible actions to

achieve net zero carbon emission

by 2050."

Meeting this target is certainly a big

challenge. Around 67% of Hong

Kong's carbon emissions come from

the power sector and around 50%

of electricity is generated by coalfired

power plants which incur the

highest carbon intensity. So, the

power sector is critical.

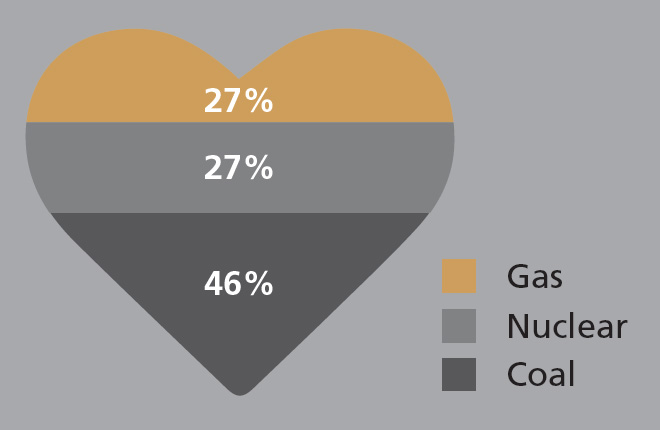

The Hong Kong energy mix in 2017

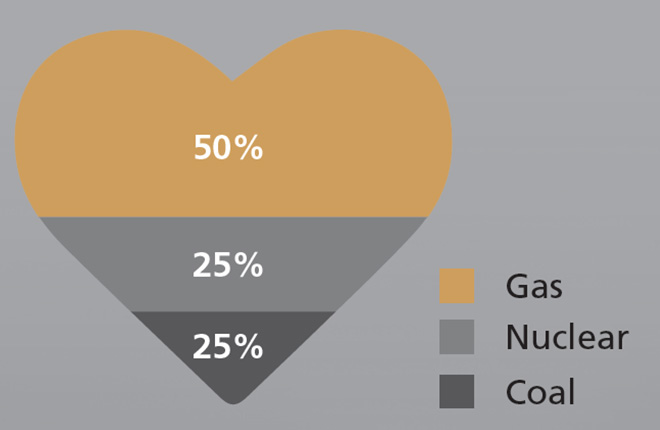

The Hong Kong energy mix target for 2020

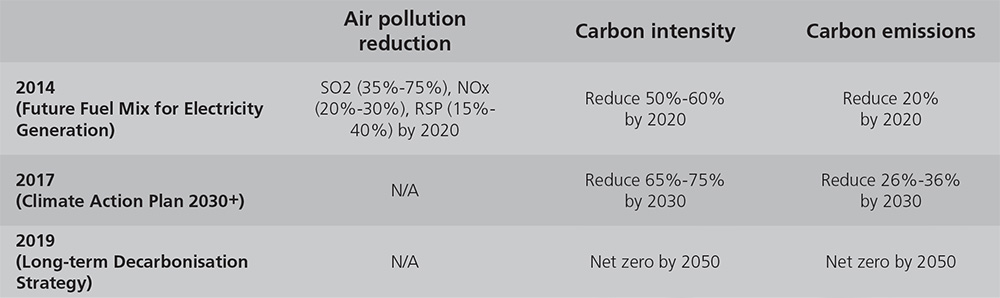

Curbing air pollution and

carbon emissions (2014-2020)

The Hong Kong government first

targeted air pollution reduction by

means of using relative "cleaner"

natural gas in electricity generation.

Then, carbon emissions reduction

became the major target for

combating climate change (Climate

Action Plan 2030+).

| Hong Kong plans 80% nuclear and renewables by 2050 |

|---|

|

To achieve a carbon reduction target of well below 2°C in 2050 that

is in compliance with the Paris Agreement, it is estimated that about

80% of our electricity would need to come from zero carbon energy sources (including renewable energy and imported nuclear energy).

As Hong Kong has very limited renewable energy potential, regional

cooperation plays a crucial role in helping us achieve a higher carbon

reduction target beyond 2030.

Public Engagement Document, June 2019

|

The limits of coal-fired

generation

Hong Kong's electricity sector

has always been privately-owned

and operated, and is run by

two vertically-integrated power

companies, Hong Kong Electric

(HKE) and China Light and Power

(CLP). HKE provides about onequarter

of the territory's power

to Hong Kong Island and Lamma

Island, whilst CLP provides around

three-quarters of the total to the

New Territories, Kowloon and

most of the outlying islands. The

two companies are regulated

under a Scheme of Control (SoC)

Agreement with the government which is periodically renewed.

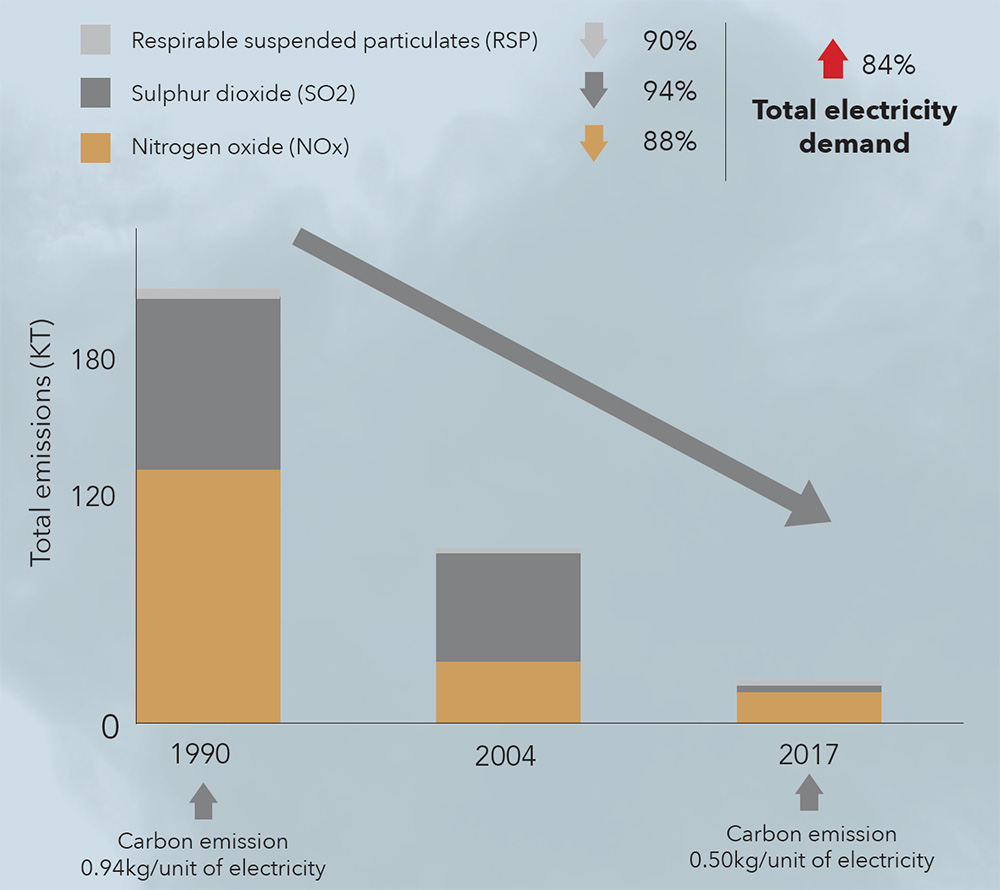

Back in 1997, the Hong Kong

Government decided not to build

any new coal-fired power plants.

The idea was to reduce particulate

matter, SO2 and NOx, and to

resolve the air pollution problem.

Any retired coal-fired power plants

were to be replaced by natural gasfired

power plants. This strategy

was based on natural gas being

considered a kind of relatively

"clean" energy, and has seen

dramatically improved pollution

performance at CLP.

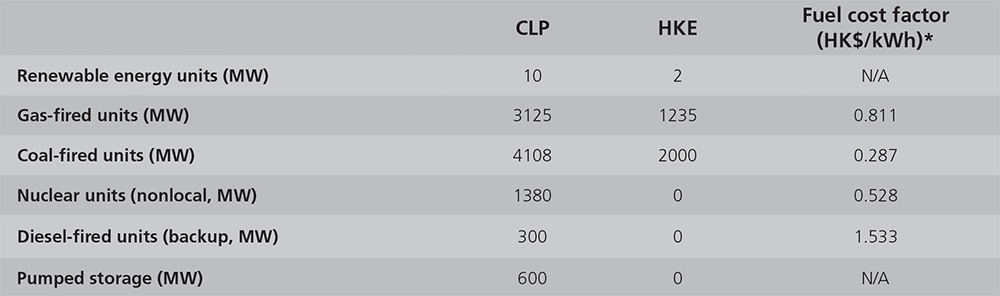

In order to meet the targets set in

2014 and 2017, Hong Kong began

to replace coal-fired power plants

with gas-fired. The generation

capacity of the two power

companies in 2018 is summarised

by fuel type in the table on the

facing page.

There were ten gas-fired power

plants satisfying 27% of electricity

requirements in 2017. SO2 and

NOx have been greatly reduced

at CLP, which supplies around

77% of Hong Kong's electricity

requirements.

Progressive reduction of emission target (base year 2005)

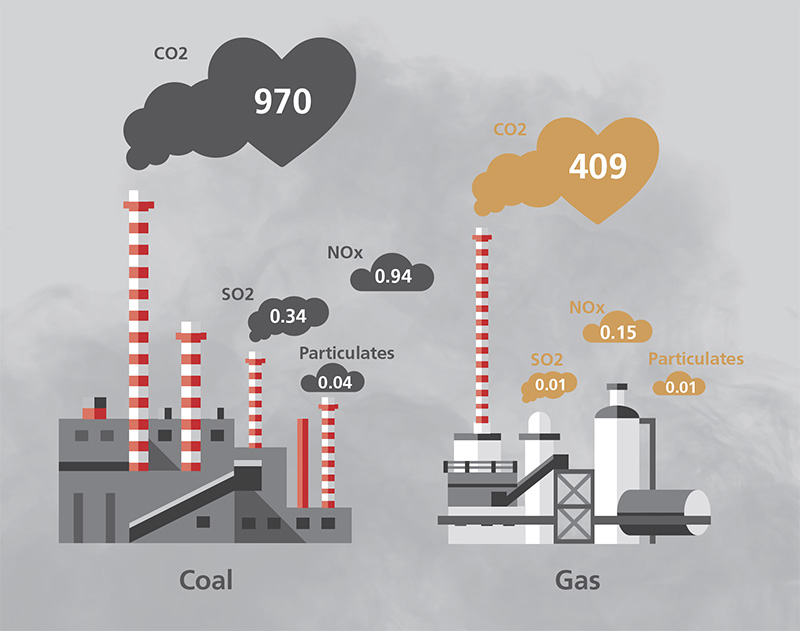

Emissions from CLP generation units in 2018 (g/kWh)

Generation capacities of Hong Kong power companies

* Source: https://www.clp.com.hk/en/community-and-environment/green-tools/energy-costs (May 2019)

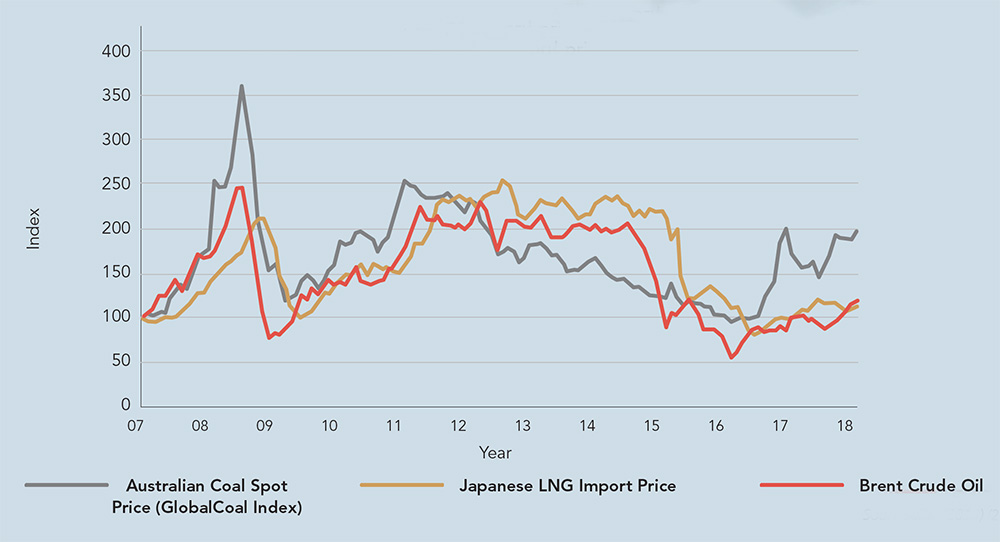

In this replacement process, Hong

Kong faces two major challenges.

First challenge – increased fuel costs

The fuel for electricity generation is

imported and the fuel cost factor

of a gas-fired unit is around three times that of a coal-fired unit.

Consequently, using more natural

gas means that the electricity tariff

will increase sharply. Hong Kong is

facing significantly higher costs to

curb air pollution. Added to that,

fuel prices are volatile as shown in

the index below.

CLP total emissions 1990-2017

Source: CLP (2018)

Second challenge – diversification of LNG fuel

sources

CLP has two main gas supply

sources, the Yacheng Gas Field near

Hainan Island, China which has

been used since 1996 and is nearly

exhausted, and the Second West-

East Gas Pipeline (WEPII) which

came on stream in 2013. This is the world's longest gas pipeline

crossing 14 provinces of China.

HKE, on the other hand, has

a steady supply of LNG from

Australia's North-West Shelf and Qatar. The LNG is shipped to

Shenzhen where LNG is gasified

and delivered to HKE by pipeline2.

When CLP's Yacheng Gas Field is

exhausted, it will rely on a sole LNG supplier. This is not good

business practice, especially given

the increasing role of gas-fired

generation in the Hong Kong mix.

This vulnerability of supply was

highlighted when CLP encountered

a two-month suspension of gas

supplies from WEPII due to a

landslide in Shenzhen in December

2015. As a result, CLP needed to

use more coal-fired power plants

and this affected its air pollution

performance. So, the diversification

of gas sources is an important issue.

Fuel price index of CLP

Source: CLP (2018)

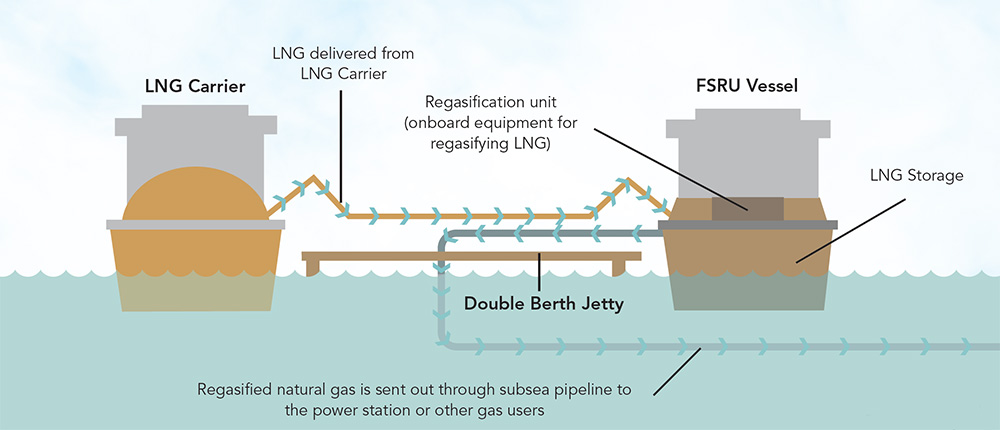

A global LNG market

To resolve the challenges of gas

price stability and supply security,

the two power companies have

proposed to build an offshore LNG

terminal. This uses state-of-theart

Floating Storage Regasification

Units (FSRU) to enable direct

purchase of LNG from the

international gas market.

| A global LNG market |

|---|

|

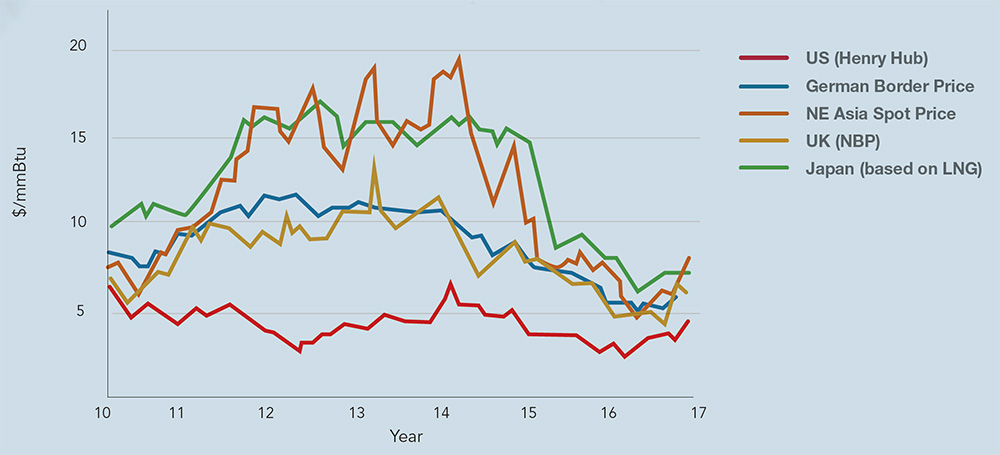

The natural gas market is becoming more globalised, and is rapidly

changing as can be seen in the divergent prices of natural gas in 2011-

2016. For example, in 2012, the spread between NE Asia average spot

price at around US$15 and UK average price was about US$5/mmBtu.

To investors, such kind of price divergence was extremely important

because it is closely monitored by spot suppliers of liquid natural gas. In

order to maximise these suppliers’ profit, they would look to ship their

liquid cargoes to the most profitable destinations, typically NE Asia and

Japan.

The convergence of natural gas prices will speed up with the maturity of

trading hubs and the increasing capacities of LNG's production facilities

and cargoes. Since 2016, average gas prices in NE Asia and Japan have

been around US$6/mmBtu, while US prices were around $3.5/mmBtu,

illustrating the relatively narrow global price range. Obviously, there

must be a price gap between US and Asia due to the varying shipping

costs.

Price convergence has caused two significant changes in the gas market:

shorter contract periods and the delinking of gas and crude oil contract

prices. According to the International Gas Union, there is a gradual shift

from long-term (5+ years), fixed destination contracts to short-term (less

than 2 years) and medium-term ones (2-5 years), due to an increase in

the number of contracts that have the flexible destination option and also

due to the emergence of new producers and consumers. For contract

prices, historically, natural gas prices have been indexed to the price of

crude oil and therefore most gas contracts use an oil price as the main

index. Recently however, natural gas prices have been increasingly

delinked from crude prices, with the potential to get much cheaper.

|

Convergence of LNG prices

Source: https://www.igu.org/resources-data

Floating Storage Regasification Units

Source: CLP (2018)

An understandable concern for

Hong Kong residents is if there is access to an international

gas market right now, why is

there a need to build this new

infrastructure? This is because the

profit of power companies in Hong

Kong is determined by the Scheme

of Control Agreements3,4 with the

government. Profit is equal to the

permitted rate of return for each

year and this is capped at 8% of

the total value of their Average Net

Fixed Assets for that year. That is,

the profit of the power companies

relies upon how many fixed

assets the companies have built.

Consequently, the power companies

are constantly interested in

investing in more fixed assets, such

as the FSRU, in order to generate

more profit. The effectiveness of

FSRU in terms of gas price stability

and supply security is not the key

concern of the power companies.

Hence, we should take a look at the

development of the LNG market

and check if using an offshore LNG

terminal is effective in the near

future. We conclude, as long as the

LNG's prices are globally converging and the infrastructure of the LNG's

market is becoming mature, the

effectiveness of FSRU is justified.

How Hong Kong can meet net zero carbon emissions by 2050

While Hong Kong had been

putting some effort into curbing

air pollution and reducing

carbon emissions, an urgent and

challenging target emerged:

achieving net zero carbon emissions

by 20505. To achieve this carbon

neutral state, various international

cities and countries have set

strategies such as6:

- Enhancing education and public awareness to reduce

consumption

- Enhancing building energy efficiency – for example, energy saving works (e.g. retrofitting and retro-commissioning) mandatory for all existing large buildings, and mandating all new buildings to be net zero carbon emissions

- Promoting green transport – such as mandatory zero emission vehicles to replace all conventional fuel-driven vehicles

- Deep decarbonisation in the energy (power) sector – such as using renewable energy and nuclear energy as the major energy sources, supplemented by fossil fuel generation equipped with carbon capture and storage technology

- Technological breakthroughs – rigorous technological breakthroughs and advancements to reduce and offset carbon emissions

Indeed, decarbonisation in the

energy sector is the most critical

pathway. Enhancing building

energy efficiency alone cannot

achieve a net zero target although

90% of electricity consumption is

from buildings. Promoting green

transport implies accelerating

the adoption of electric vehicles,

which pushes the emissions back

to the power plants. Hence,

not surprisingly, the Hong Kong government proposes to use

nuclear and renewable generation

(solar and/ or wind) as the

major energy sources. Nuclear

and renewable generation are

generally considered as having a

"virtual" zero carbon emission.

However, even nuclear energy

and photovoltaics have a certain

amount of lifecycle green house

gas emissions compared to other

renewables. But, other concerns

may negatively affect Hong Kong in

the adoption in achieving the zeroemission

target.

Fukushima and worldwide opposition to nuclear power

The increased use of nuclear

energy, may be constrained by

public concerns. The nuclear energy

currently imported from mainland

China contributes around 25% of

Hong Kong's electricity supply. In the

2014 consultation document (Future

Fuel Mix for Electricity Generation),

the government proposed to import

more nuclear from mainland China,

but met with societal concerns due

to the 2011 Fukushima incident.

Indeed, if we look internationally,

four regions have undertaken to

end nuclear power generation

completely – Germany, Switzerland,

Belgium and Taiwan.

How about renewables? Land

scarcity does not allow Hong

Kong to deploy large-scale solar

or wind farms, and offshore busy

sea lanes ensure that wind farms

are impossible. In June 2019, the

Hong Kong government published

Public Engagement on Long-term

Decarbonisation Strategy7, where

it is estimated that according to

current technologies, there are

only modest realisable renewables

including solar, wind, and wasteto-

energy at about 3%-4% of total

demand, by 2030. The government

therefore proposes regional

cooperation allowing Hong Kong

to tap into renewables available in

mainland China.

Note that the government also

considers that importing more

nuclear energy from mainland

China is a kind of regional

cooperation. The existing

connecting grid is being enhanced

to supply around 30%-35% of

Hong Kong's fuel mix.

A carbon neutrality coalition

The effectiveness of regional

energy cooperation around the

world is well documented in

the government's consultation

publication. For instance, there

are interconnective grids between Norway, Sweden and Germany

allowing Denmark to export

excessive wind power when

necessary, and to import Norwegian

hydropower, Swedish nuclear

power and German solar power

when the wind is still.

Obviously, this kind of regional

cooperation is not comparable to

that proposed by the Hong Kong

Government in the engagement

document, in which Hong Kong

invests in nuclear and renewable

generation capacity in mainland

China and transmits the power to

Hong Kong. In terms of energy

policy, it is not a good practice,

as mainland China also requires

green generation to meet the net

zero emission target. Although the

government's energy policies have

considered the criteria of reliability,

security and availability, and

affordability, the more appropriate

energy policies should include the

consideration of "equity". That is,

we need to consider if Hong Kong's

energy policies negatively affect the

"reliability, security and availability,

and affordability" of mainland

China's power market. Currently,

the more power is imported from

mainland China to Hong Kong, the

more unreliability is imposed on

China's power system and end users.

Moreover, if the government

insists on the proposed regional

cooperation, it should be aware

that the technologies of power

systems are enhancing rapidly, for

example in intelligent grid systems

and ways to store electricity, such as

giant battery plants. It is therefore

recommended that such kind of

cooperation should be revised every

five years to meet the 2050 target.

Instead of considering regional

cooperation through importing

predominantly nuclear generation

capacity, we should explore other

viable alternatives, such as a carbon

neutrality coalition.

The importance of planting trees

Although land scarcity prevents

Hong Kong from implementing a

carbon sink strategy locally, we may

still consider the path of carbon

neutrality8 by means of planting of

trees in the Belt and Road countries and mainland China thereby

obtaining a carbon credit to offset

Hong Kong's carbon emissions9.

Indeed, mainland China can initiate

a Carbon Neutrality Coalition10

for Belt and Road countries.

With Hong Kong's investment in

offsetting carbon emissions, China

could develop a Green Belt and

Road. Note that reducing emissions

from deforestation and forest

degradation in developing countries

is also a kind of carbon neutrality11.

IPCC12 presents a research output

that the carbon neutrality potential

is estimated up to 23 GtCO2

dominated by reduced rates

of deforestation, reforestation

and forest management, and

concentrated in tropical regions.

A green future

Assuming that Hong Kong uses

gas-fired power plants to supply the

63,000 million kWh consumption

requirement in 2050 (this implying

around 1% increase annually), with the current emission factor

(488gCO2eq/ kWh), Hong Kong

needs to offset 30.8 million tonnes

CO2e which would require planting

around 52 times Hong Kong's land

area13. According to Pakistan's

cost factor14, current marginal

abatement cost (US$/tCO2e

reduced) is around $10 to $25.

The estimated offsetting cost for

Hong Kong from now until 2050 would be around US$308 million

to US$770 million at current US$

prices in total. With 68 Belt and

Road countries to plant trees in,

there is plenty of scope for Hong

Kong to start the carbon neutral

process now and meet the future

net zero emission target by 2050.

Assuredly, this kind of "regional

cooperation" would result in a winwin

situation.

Greta Thunberg, the 16-year-old climate activist from Sweden, sails into New York Harbour flanked by a fleet of 17 sailboats representing each of the United Nations Sustainable Development Goals on their sails

Courtesy of the UN Photo by Mark Garten

How about Hong Kong?

How should we generate power?

Gas, nuclear, renewables?

What do you think?

"Changing one disastrous

energy source for ‘a

slightly less disastrous

one’ is not progress"

Greta Thunberg climate activist

| Carbon sinks |

|---|

|

Carbon sinks are natural systems that soak up and store CO2 from the

atmosphere. Forests are great examples. During photosynthesis, trees

and plants sequester or absorb CO2 from the atmosphere, using it as

food for growth. The carbon from the CO2 becomes part of the plant

and is stored as wood, stems and leaves. Although forests do release

some CO2 in their natural succession, a healthy forest typically stores

carbon at a greater rate than it releases carbon.

The existing carbon sink in Hong Kong is only about 1% of the

total carbon emissions, hence the importance of a regional carbon

neutrality policy.

Public Engagement on Long-term

Decarbonisation Strategy, 2019

|

| What are carbon offsets? |

|---|

|

A carbon offset is a reduction in emissions of carbon dioxide or

other greenhouse gases made in order to compensate for emissions

made elsewhere. Offsets are measured in tonnes of carbon dioxideequivalent

(CO2e). One tonne of carbon offset represents the

reduction of one tonne of carbon dioxide or its equivalent in other

greenhouse gases.

Offsets typically support projects that reduce the emission of

greenhouse gases in the short or long-term. Common project types

are renewable energy, energy efficiency and forestry projects.

|

| The potential for global forest cover |

|---|

|

The restoration of forested land at a global scale could help capture

atmospheric carbon and mitigate climate change. Bastin et al. used

direct measurements of forest cover to generate a model of forest

restoration potential across the globe. Their spatially explicit maps

show how much additional tree cover could exist outside of existing

forests and agricultural and urban land. Ecosystems could support

an additional 0.9 billion hectares of continuous forest. This would

represent a greater than 25% increase in forested area, including more

than 500 billion trees and more than 200 gigatonnes of additional

carbon at maturity. Such a change has the potential to cut the

atmospheric carbon pool by about 25%.

Science, July 2019

|

References:

Dr William Chung

Associate Professor

Department of Management Sciences