Dr Zilong Zhang, Assistant Professor in the Department of Accountancy, looks at the

chequered history of China's state-owned enterprises and how a series of defaults brought a

systemic response and increased financial discipline to the sector. This article is based on "The

Value and Real Effects of Implicit Government Guarantees," by Shuang Jin, Wei Wang, and

Zilong Zhang, May 2017.

State-owned enterprises (SOEs) are

systematically important in China's

economy, helping to create and

maintain millions of jobs, as well

as support strategically important

industries. Historically, publicly-listed

SOEs have contributed up to

85% of the total sales of all listed

companies in China1, and were

widely seen as being "too big to

fail." But behind the impressive

statistics opinion remained divided

on the efficiency of the state-owned

sector. In the early 2010s

sentiment began to change. At the

fourth meeting of the US-China

Strategic and Economic Dialogue

(S&ED) in May 2012, China

committed to "developing a market

environment of fair competition for

enterprises of all kinds of ownership

and to providing non-discriminatory

treatment for enterprises of all

kinds of ownership in terms of

credit provision, taxation incentives,

and regulatory policies." The winds

of change seemed to be gathering

force over the SOE sector. Was

accountability now to be the name

of the game?

Investors cling to the old

belief in implicit government

guarantees

Initially, investors were not too

bothered. They clung to the belief

that SOEs were simply "too big to

fail." When these often gigantic

companies were in danger of

default, the government had always

somehow found a way to bail

them out. After all, back in 1997,

when Jiangxi Radio Factory was on

the verge of bankruptcy, the local

government had invited Tsinghua

Tongfang, a software company

based in Beijing, to acquire the

factory and inject capital into the

merged firm. The government

provided policy support for the

merger and the debt repayment.

Again, in 2008, the central

government – in the form of the

State-owned Assets Supervision and

Administration Commission – had

directly subsidised five state-owned

electricity companies that were

deeply distressed. The subsidies

shared by the five companies

amounted to a then massive USD

1.8 billion in total.

Such "implicit government

guarantees" created a safe harbour

not only for SOEs' bond investors, but also for their managers. In

anticipation of a government

guarantee, managers tended to

borrow excessively and overinvest

in inefficient projects without

worrying too much about the

consequences. Such implicit

government guarantees were

criticised as an important cause

for the high financial leverage of

SOEs' overcapacity and inefficient

production.

The unprecedented credit boom of

the early 2010s further aggravated

the overleverage and overcapacity

problems. According to the China

Stock Market & Accounting

Research (CSMAR) database, during

2011-2015, the financial leverage

of SOEs averaged 54% while the

average return on assets of SOEs

was only 3.3%. The corresponding

numbers for non-SOEs, however,

were a rather more financially

competitive 39% and 5.7%. To

deal with these problems, Chinese

regulators encouraged firms to deleverage

and called for the cutting

of inefficient production. A series

of non-bailout events were to

follow, reflecting the government's

declining tolerance for non-performing

firms and its attempt to

allow market forces to play a more

decisive role in restructuring the

economy.

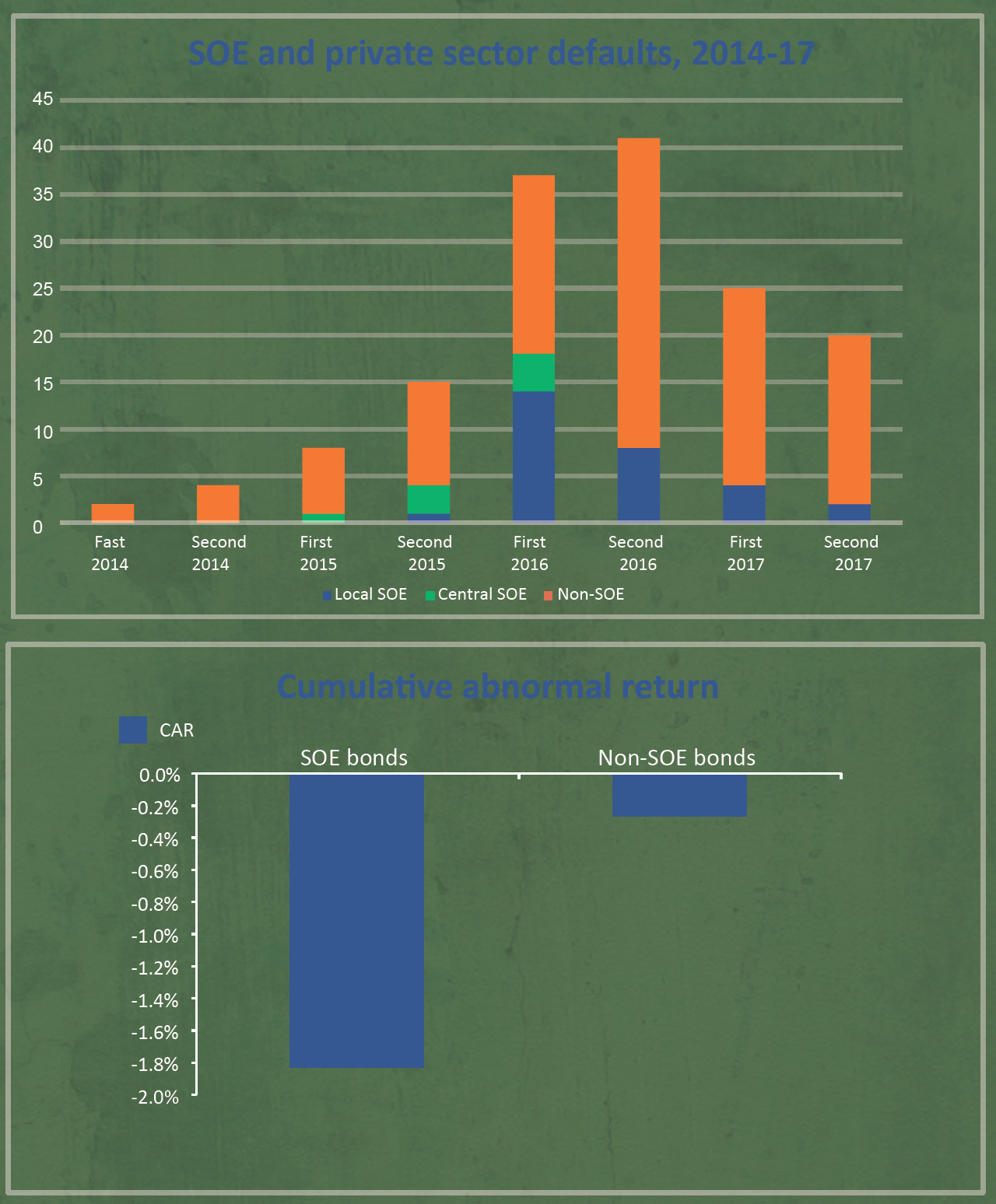

The average cumulative abnormal return of SOE bonds during a 60-day window

around the Tianwei default

"The first-ever SOE

default symbolised the

end of an era.

The implicit guarantee

had fallen through the

trapdoor of history"

The historic default of Baoding

Tianwei

The first major shockwave to hit

was on 21 April 2015. Baoding

Tianwei, a manufacturer of power

transmission and distribution

equipment including the

strategically important photovoltaic

and wind power sectors based in

Hebei province, defaulted on one

of its onshore bonds. Tianwei was

a wholly-owned subsidiary of China

South Industries Group, an SOE

ranked 102nd in the Fortune Global

500 in 2016. This was the first-ever

SOE default in the entire history

of Chinese onshore bond market,

and it came to symbolise the end of an era. The implicit guarantee

had fallen through the trapdoor of

history.

A series of SOE defaults followed

in quick succession. In July

2015, Jilin Grain Group, a grain

producing enterprise owned by

the Jilin government, defaulted

on its private placement bonds. In

September, China National Erzhong

Group, a heavy machinery company

owned by the central government

and located in Sichuan Province,

defaulted on a medium-term note

issued in 2012. In October, Sinosteel

Corporation, a mineral processing

and steelmaking company owned by the central government and

headquartered in Beijing, failed to

pay interest due on 2 billion CNY

notes maturing in 2017. And in

December, Tianwei defaulted again,

this time on one of its private

placement notes. The wave of SOE

bond defaults continued in the

following couple of years. In the

aftermath of the Tianwei default,

Moody's stated, "Recent episodes

of SOE distress show that regional

and local governments' autonomy

to provide direct financial support

to struggling SOEs is diminishing

as a result of restrictive central

government regulations."2

The retreat of the government's

guarantee came as a shock to the

corporate bond market. Investors

reacted by bidding down the price

of SOE bonds. Using the data

provided by CSMAR and WIND, we

have calculated that the average

cumulative abnormal return (CAR)

of SOE bonds was 1.53% lower

than that of non-SOE bonds during

a 60-day window around the

Tianwei default.

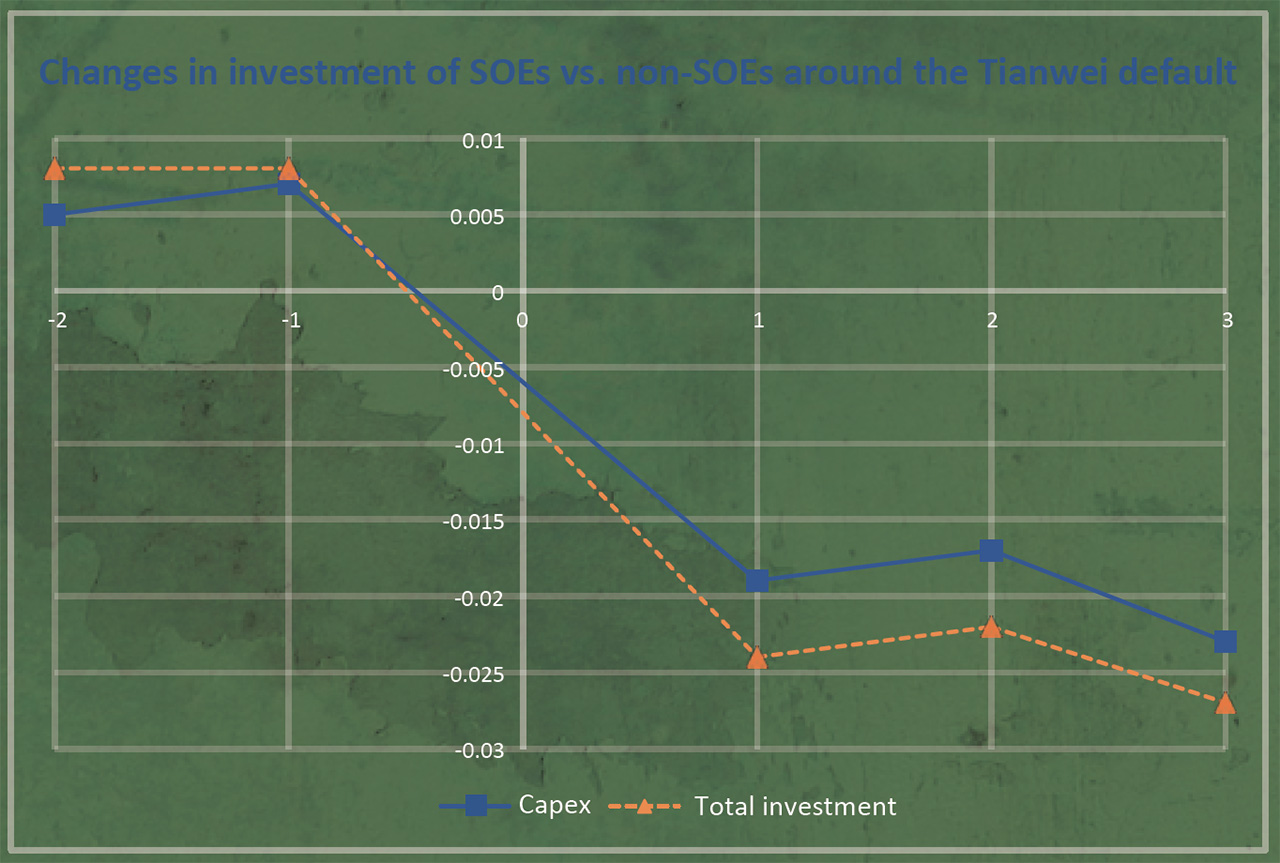

The behaviour of SOE managers

begins to change

Now the SOE managers faced a

real threat of corporate failure.

Would the threat discipline the

managers and discourage them

from making bad investment

decisions? We answered this

question by conducting regression

analyses using a large sample of

SOEs and non-SOEs from January

2013 to December 2016. We

first matched SOEs and non-SOEs

based on various financial metrics

and then examined the change in

the SOEs' investment record from

before to after the Tianwei default

relative to the change of non-SOEs'

investment in the same period.

We found that SOEs cut their

investment by 1.9% of book assets

relative to non-SOEs in the first

semiannual period after the Tianwei

default. We further split our sample

into different groups according

to manager characteristics and

performed an analysis for each

group. Interestingly, we found

that the investment reduction was mainly made by bad managers

(characterised as those managers

with above median misconducts

or lawsuits recorded against them

before the Tianwei default). Finally,

we found that SOEs managers

made better acquisitions after the

Tianwei default, as evidenced by a

better stock price reaction to their

acquisition announcements. SOE

acquirers' abnormal stock returns

outperformed non-SOE acquirers'

by 2.4% in the 5-day window

around acquisitions.

The advent of financial

discipline

Overall, our findings suggest that

the reduction of implicit government

guarantees, or the disappearance

of "too big to fail," disciplined

corporate managers. This finding not

only confirms theoretical predictions

by academia, but also has important

policy implications – allowing the

market mechanism to play its role

in restructuring troubled SOEs has a

positive effect on the real sector in

the long-run, even though it may bite

current bondholders.

"Too big to fail" is not a

phenomenon exclusive to China.

The experience of GM and Chrysler

during the 2008-2009 financial

crisis highlights the prevalence of US

government support in bailing out

systemically important corporations

during severe economic downturns.

Other real-sector firms that have

been bailed out by their home

governments include Groupe Bull

SA (France), Norilsk Nickel (Russia),

Bangkok Land (Thailand), Malaysian

Airline System (Malaysia), Railtrack

(UK), etc. In this sense, the effect

we document can travel around the

world.

References:

Dr Zilong Zhang

Assistant Professor

Department of Accountancy