Dr Stephen Sun, Assistant Professor in the Department of

Accountancy, shows how technology links among firms can help

investors predict stock returns. This article is based on "Technological

links and predictable returns," by Charles Lee, Stephen Sun, Rongfei

Wang, Ran Zhang published in the Journal of Financial Economics,

June 2019.

In today's knowledge-based

economy, technological prowess is

becoming an increasingly important

determinant of firms' short-term

profitability as well as long-term

survival. Many of the largest firms

in the world such as Amazon,

Google, Intel, and Samsung, may

have minimal overlap in product

space, yet are closely-aligned in

terms of technological expertise.

These technological affinities

transcend traditional industry

boundaries and are typically not

readily discernible from firms'

financial reports. Nevertheless, they

can be key drivers of the economic

fortune of today's businesses.

Our paper entitled "Technological

Links and Predictable Returns"

exploits this special type of inter-firm

linkage and applies this insight

to predict stock returns in the US

equity market.

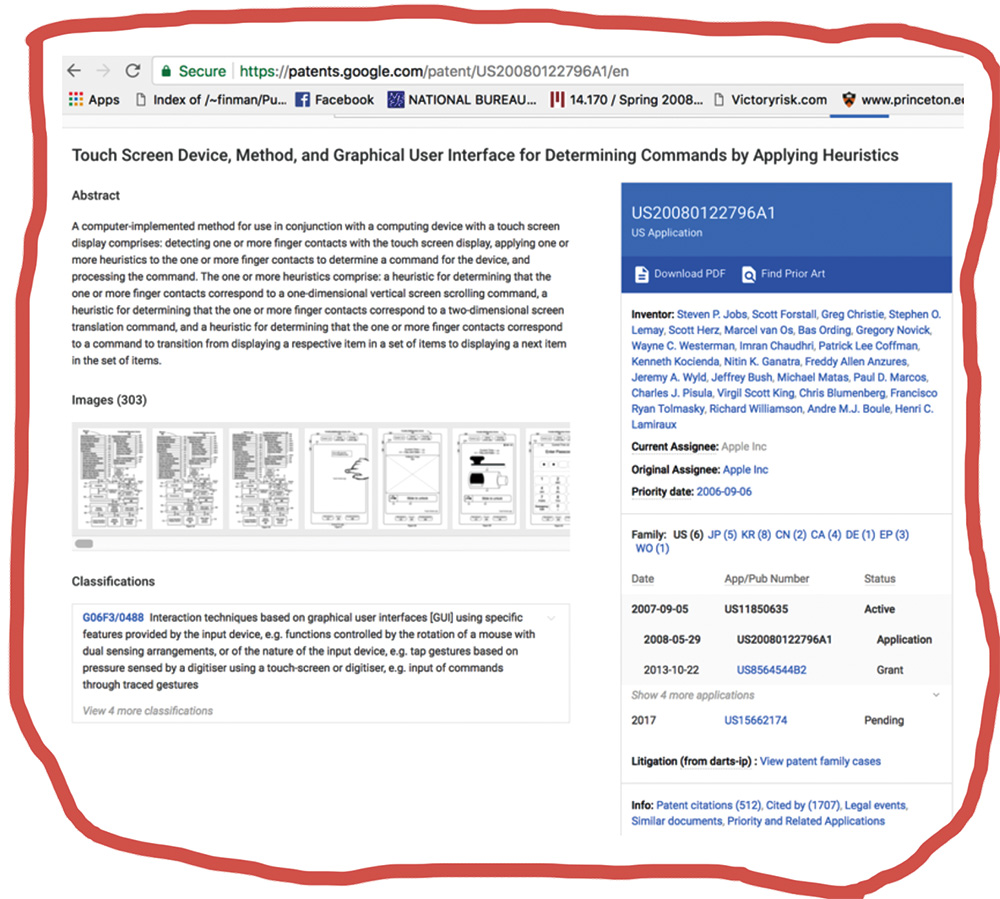

The "Steve Jobs' patent"

The inter-linkage of firms'

technologies has been around for

some time. Let's consider the so-called

"Steve Jobs' patent." This

patent basically opened the door

for the creative production of

smartphones as we know them

today. It is entitled "Touch Screen

Device, Method and Graphical

User Interface for Determining Commands by Applying Heuristics."

We can see a screenshot of the

patent information from the Google

Patents website above. It is indeed

the core patent of Apple's multi-touch

technology and has been

cited and used in countless devices

that have a multi-touch screen. This

patent is nicknamed "The Steve

Jobs' patent" as he is listed as the

first co-inventor on the patent filing

form and has been cited over 1000

times since its approval in 2009.

The patent is so valuable that it has

even received litigation to contest

and invalidate it. It was initially

invalidated in December 2012 and

finally revalidated in October 2013.

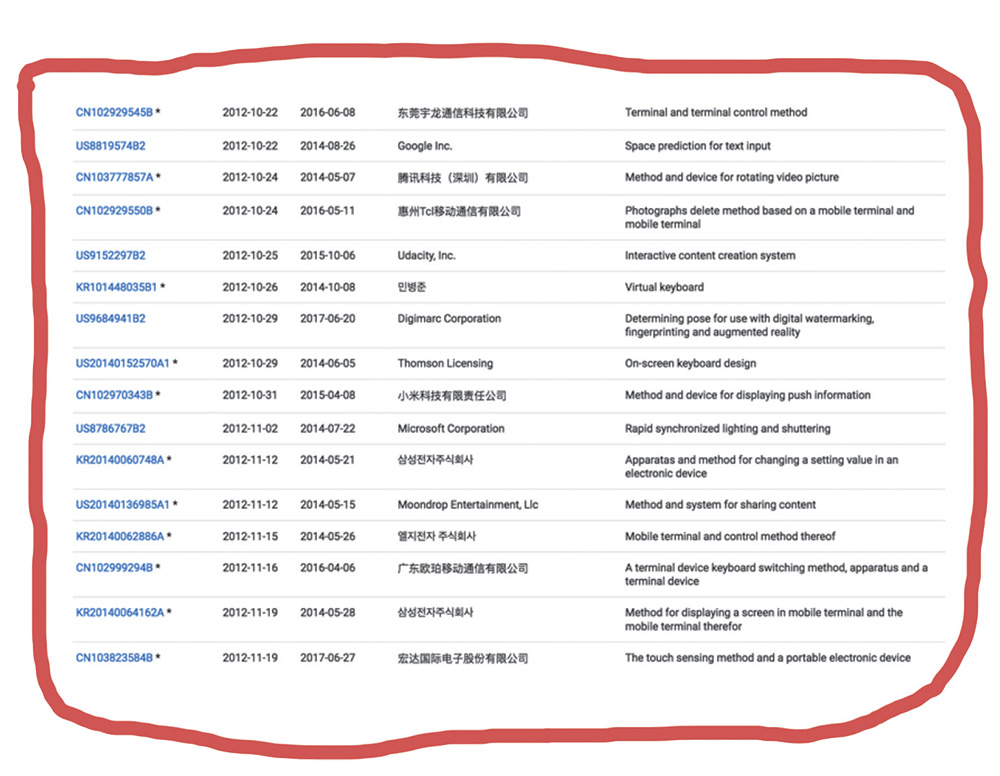

Patent citations reveal

knowledge flows among firms

We can see a screenshot of follow-on

patents by other companies

that cited this patent on the next page. Patent citation can give us

a concrete way to see knowledge

flows or technology linkages

among firms. We observe a broad

range of companies around the

globe citing this patent, from well-known

companies such as Google,

Microsoft and Tencent, as well as

companies in related electronics

sectors in China, South Korea and

the US. All these companies can be

regarded as technologically linked

to Apple in this respect.

The value of investigating

firms' technology linkages

There are two major reasons why

firms' technology linkages can

actually be useful in transmitting

values and helpful in predicting

stock returns. First, firms working

on areas of innovation that

substantially overlap with each

other could be subject to similar input or output linkages, which

become important transmission

channels for common price shocks.

For example, breakthroughs in

production technology have led

to dramatic cost reductions in

silicon chips, which in turn greatly

impacted on the vitality of the

electronics industry relying on these

chips as a raw material. Similarly,

technological progress in touch

screen technology today bodes well

for the firms making products that

use these touch-screens.

The second reason is that, firms

with similar technologies can also

benefit from the spillover effect

of each other's innovation activity

along technological lines. More

specifically, firms working on similar

technologies may use similar inputs

of production, with inputs being

broadly understood as anything

required in the production process,

for example human resources,

key raw materials, production equipment, information and

communication technology, or

intangible knowledge.

Scientific critique of new

technology can directly impact

share price

Here is a concrete real-world

example to illustrate the point.

CRISPR is a new bio-technology

that can enable scientists to edit

genes and has wide applicability. It

is believed by some to be the most

important biological breakthrough

in the past decade. However, the

technology itself is still in an early

stage and rapidly developing. A

letter in the renowned journal

Nature Methods on 30 May, 2017

pointing out potentially dangerous

flaws in the CRISPR-Cas9 gene

editing system, gave biotech

investors a sinking feeling that

day and stocks in genome-editing

companies using that technology

had the same experience. By the

close of trading Editas Medicine had fallen nearly 12 percent, Crispr

Therapeutics was down just over 5

percent, and Intellia Therapeutics

had plunged just over 14 percent.

All these bio companies relied

upon technology very similar to the

CRSPR technology.

A similar event happened again

on 8 January 2018. The world

of science awoke to news that

suddenly cast uncomfortable

doubt on many of the past five

years' major breakthroughs: A new

paper had identified a possible

barrier to using the revolutionary

gene-editing tool CRISPR-Cas9

in humans. The news incited a

temporary hysteria that sent the

stocks of all three major CRISPR

biotech firms tumbling in premarket

trading, declining by as much as

11.9 percent.

How to exploit inter-firm

technological linkages to make

profits

In our paper, we find that

investors can exploit the inter-firm

technological linkages to make

profits in the equity market. The

idea is very simple. For each firm,

we can identify a set of companies

to which it is technologically

related in terms of their patenting

similarities. We call such closely

related companies "technology

peers." We then calculate the

average stock return in the past

month of these technology peers.

We then sort firms at the beginning

of each month according to the

average stock return of their

tech peers. We will buy those

firms above 90% most profitable average tech peer returns and

short sell those firms below 10%

most profitable average tech peer

returns, in equal weighting. This

turns out to be a very profitable

investment strategy, generating a

mean annual return over 14% and

is quite robust, with T-statistics over

5. We also explore the underlying

mechanisms for this strong asset

pricing anomaly result. We find

the results are driven by investors'

limited attention bias, consistent

with a growing behavioral finance

literature that documents similar

patterns. That is, investors do not

seem to pay enough attention to

the timely change in technologically

related firms' stock price changes.

As the technologically related firms

convey value-relevant information

to the focal firm, ultimately the

focal firm's stock price will move in

similar directions to their technology

peers.

Greater attention to

technology-linkages leads to

better investment decisions

Our study matters as it points

to researchers needing to better

understand the mechanism through

which such technological attributes

impact information processing

costs, and thus market prices. In

our own words: "It is difficult to

argue that this publicly available

mapping should not be taken into

account when forming expectations

about technology-intensive firms'

future cash flows. Certainly, from

an investor's perspective, greater

attention to technology-linkages

could lead to better investment

decisions. From a firm's perspective,

educating investors on its

technological capabilities, perhaps

through greater media coverage,

may likewise yield improvements in

pricing efficiency."

A note from the author

The paper, "Technological Links

and Predictable Returns" was

coauthored with my former

colleague Professor Rania Zhang

and PhD student Rongfei Wang

at Peking University, Guanghua

School of Management, as well as

Professor Charles Lee at Stanford

University, where I obtained

my PhD in economics in 2015.

The paper was published in the

2019 June issue of the Journal of

Financial Economics and has won

the 2018 Roger F. Murray Prize

by The Institute for Quantitative

Research in Finance, also known

as the Q-group. The work is not

only published in a world-class

academic journal, but has also been

well received in the investment

community. While our study only

uses data from the US stock market,

some Chinese hedge funds have

replicated our results and applied it

in the China equity market.

Dr Stephen Sun

Assistant Professor

Department of Accountancy