欲於待, 則書之成未有日也

宋, 戴侗, 《六書故》

Were I to await perfection, my book would never be finished

Dai Tong, History of Chinese Writing, Song Dynasty

Professor Houmin Yan, Chair Professor of Management Sciences, and Director, Hong Kong Laboratory for AIPowered

Financial Technologies Ltd. charts the chequered history of alternative data, ensuing concerns over data

privacy, and how a federated learning model working in the context of supply chain finance can provide rich and

transparent alternative data.

I clearly remember my

excitement at the news of

AlphaGo defeating the top

human Go players.

I clearly remember my excitement

at the news of AlphaGo defeating

the top human Go players back

in 2017. To crack this complicated

game, AlphaGo used 300,000

games to train the model. The

occasion had been anticipated by

an article about mastering the Go

game with deep neural networks

published in Nature the previous

year. Subsequently, another article

about applications of reinforcement

learning for Go was published

in Science. It generated great

interest among my colleagues. Jeff

Hong organised a study group on

machine learning in the college

and many young faculty and

PhD students participated. We

all hoped that with modern data

technologies, AI algorithms would

demonstrate their full potential.

However, for many industry

applications, data remained the

issue. Did we have sufficient data to

train AI? Could we answer concerns

over data security and privacy? And

in the light of these questions, were

new algorithms or computational

architecture necessary?

A detour to Cambridge

"Farewell to Cambridge,"

a poem by Chinese modern

romantic poet Xu Zhimo,

was in the back of mind.

Around this time three years ago,

I was assigned by the European

Foundation for Management

Development (EFMD) as a member

of the EQUIS peer review team

for Nova School of Business and

Economics, Portugal. It happened

that CB had an EMBA overseas

module running at Cambridge

University at the time. The overseas

module started on a Saturday and

the EQUIS accreditation started on

the following Monday. Knowing

that I had not been to Cambridge

before, my EMBA colleagues asked

me if I could make a detour. How

could I reject such an appealing

proposal? There was the famous

statute of Isaac Newton at Trinity

College to see, and besides "Farewell

to Cambridge," was in the back

of mind. This poem by Chinese

modern romantic poet Xu Zhimo,

had been with me since school

days, striving to loosen the Chinese

traditional form and to reshape

it using influences from western

poetry styles. The prospect of a visit

to historical Cambridge was alluring,

but my visit was to pull me in more

contemporary directions.

Early warning signs: Cambridge

Analytica and the expandability

of data

Facebook's default

settings allowed

Cambridge Analytica

to harvest respondents'

Facebook friends, a

dramatic example of

the expandability of

alternative data.

On the first day I attended a lecture

by Judge Business School Dean,

Christoph Loch. But regrettably, I

missed a second lecture by David

Stillwell on the use of personal

data. This was a big miss since

that week the New York Times

and the Guardian reported that

British consulting firm, Cambridge

Analytica, had obtained the

personal data of millions of

Facebook users. Stillwell and

Aleksandr Kogan had developed an

app surveying limited numbers of

Facebook users for academic use,

but Facebook's then default settings

also allowed Cambridge Analytica

to harvest respondents' Facebook

friends, a dramatic example of the

expandability of "alternative data"

in this case with significant negative

outcomes. Without user consent,

Cambridge Analytica employed the

data predominately for the political

campaigns of Ted Cruz and Donald

Trump. The scandal was widely

reported resulting in Cambridge

Analytica going bankrupt, Facebook

settling the case with billions of

US dollars, and in 2018 the EU's

General Data Protection Regulation

(GDPR) was to take effect.

Ant Group uses accumulated

transaction data for loan

approval

Ant uses accumulated

transaction data to

continuously optimise its

business decision-making

algorithms.

Another landmark instance

of the use of alternative data

relates to the Ant Group. Starting

from 2004 as Alipay, Ant Group

gradually started to provide

innovative financial services such

as financing, wealth management,

and insurance to both consumers

and companies. Their approach

differed from traditional bank loan

approval processes, which were

heavily based on a firm's financial

and accounting data, and in turn

focused on various financial ratios,

such as the ratio of the loan to the

borrower's total assets, the current

ratio, leverage ratio, and liquidity

ratio. The Ant Group's approach

uses accumulated transaction data

(alternative supply chain data) to

continuously optimise and train

its business decision-making

algorithms, thereby improving

target customer identification and

customer acquisition capabilities.

For loans, Ant Group automatically

sends repayment reminders to the

borrower, with most repayments set

to be automatically repaid through

the borrower's Alipay account.

According to investment bank

reports, the company has the right

to directly deduct both principal

and interest from the person's

Alipay account. In continuing to

expand the use of transaction

data, this alternative approach and

alternative data clearly contributed

to Ant's business model for

facilitating billions of loans. The

last-minute halting of Ant's IPO

in November 2020 was probably

another example of concerns over

data monopoly and privacy.

The regulatory agencies

suggest alternative data for

credit scoring

The most common AI

techniques have a central

data processor that

imposes risks in crosssharing

customer data.

The use of customer data has

understandably drawn the attention

of the regulatory authorities. In

November 2020, the Hong Kong

Monetary Authority (HKMA) and

Hong Kong Applied Science and

Technology Research Institute

(ASTRI) released a white paper

"Alternative Credit Scoring of

Micro-, Small and Medium-sized

Enterprises (MSMEs)." Through

Financial Technology (FinTech), the

paper argued that an alternative

approach and alternative data

could facilitate loans to small and

medium-sized enterprises. The

paper indicated: "There has yet

to be a treasure hunt to develop

models that use alternative data

for credit scoring. Machine learning

and AI techniques seem to offer the

best chance by far for the financial

industry to crack the code." The

most common machine learning

and AI techniques have a central

data processor that collects data

from various sources. However,

it imposes risks in cross-sharing

customer data. In contrast with

the traditional learning approach,

federated learning makes use of

raw data for training models to

obtain intermediate results. To

reflect a joint effort in developing useful models, rather than the

raw data, the intermediate results

are shared among raw data

contributors.

With federated learning the

data is available but not visible

Federated learning

takes advantages of

recent developments in

machine learning whilst

maintaining data security

and privacy.

For data security and privacy issues,

Google has developed a concept

of federated learning to provide

a machine learning environment

such that datasets are distributed

and data leakages are prevented.

This approach was elaborated

by Professor Yang Qiang of the

Hong Kong University of Science

and Technology, published in

"Federated Machine Learning:

Concept and Applications," in

2019. With different alternative

data sets, Yang reckons that

federated learning can be a good

vehicle, taking advantages of recent

developments in machine learning

whilst maintaining data security

and privacy.

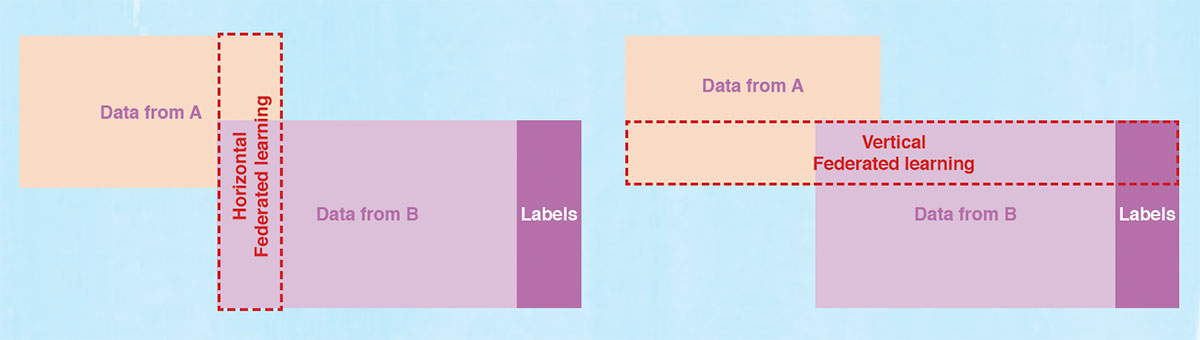

Taking a two-party machine

learning example, Yang classifies

federated learning as horizontal,

vertical, and transfer learning

based on varying data needs.

Horizontal learning applies when

similar feature data exist but data is

owned by different companies who

serve different customers. Vertical learning applies when different

feature data presents and data

is owned by different companies

who serve the same customer.

Transfer learning applies when

feature data is different and the

customers served are also different.

With federated learning structures,

the objective is to make the other

party's data available but not

visible, and to make use of other

party's data but not change data

ownership.

The key issues for the

financial industry are

expandability and the

lack of transparency of AI

technologies.

In the last few years, various

algorithms and architectures

have been proposed for financial

applications, but have generally

fallen short of the full adoption of

AI and machine learning for loan

arrangements. One could argue

that there is a lack of regulatory

guidance on the application of AI

algorithms. Obviously, current bank

systems' governance processes

for technology, digitisation, and related services deployments

might not remain fit-for-purpose

in AI-governed environments. But

the key issues for the financial

industry are probably concerns

over the expandability and lack of

transparency of AI technologies.

Safety first: Banks favour

transparent algorithms

The EU's General Data

Protection Regulation

requires AI algorithms

to explain their decisionmaking.

AI algorithms, such as deep

learning algorithms implemented

by neural networks, have been

described as a "black-box." Banks

favour transparent algorithms

characterized by clarity. For

example, if age is used as a factor

in the credit screening process

for lending in a traditional bank,

can traditional algorithms, such

as logistic regression or decisiontrees,

provide clarity on how age

has played a role in the decisionmaking

i.e., to approximate the

relationship between inputs (e.g.

age) and outputs (probability of default?). The decision-tree based

machine learning algorithm has

been considered as a promising

candidate for understanding,

interpretation, and visualisation. It

has also been widely tested as being

comparable with deep learning

algorithms, which all depend on

the nature of applications. If data is

highly structured, the decision-tree

based algorithm performs very well

in competing with deep learning

algorithms. But it may produce

complex trees and become unstable

because of small variations in data

resulting in different tree structures.

Another noticeable feature about

the decision-tree based algorithm

is the lack of support for horizontal

federated learning. Actually, in

addition to requesting data privacy

and ownership, the EU's General

Data Protection Regulation also

requires AI algorithms to explain

their decision-making. The research

frontier is therefore two-fold:

Firstly, to enhance cryptographic

operations in the decision-tree

based algorithms, and secondly to

add linear proxy models or decisiontree

structure to deep learning

algorithms.

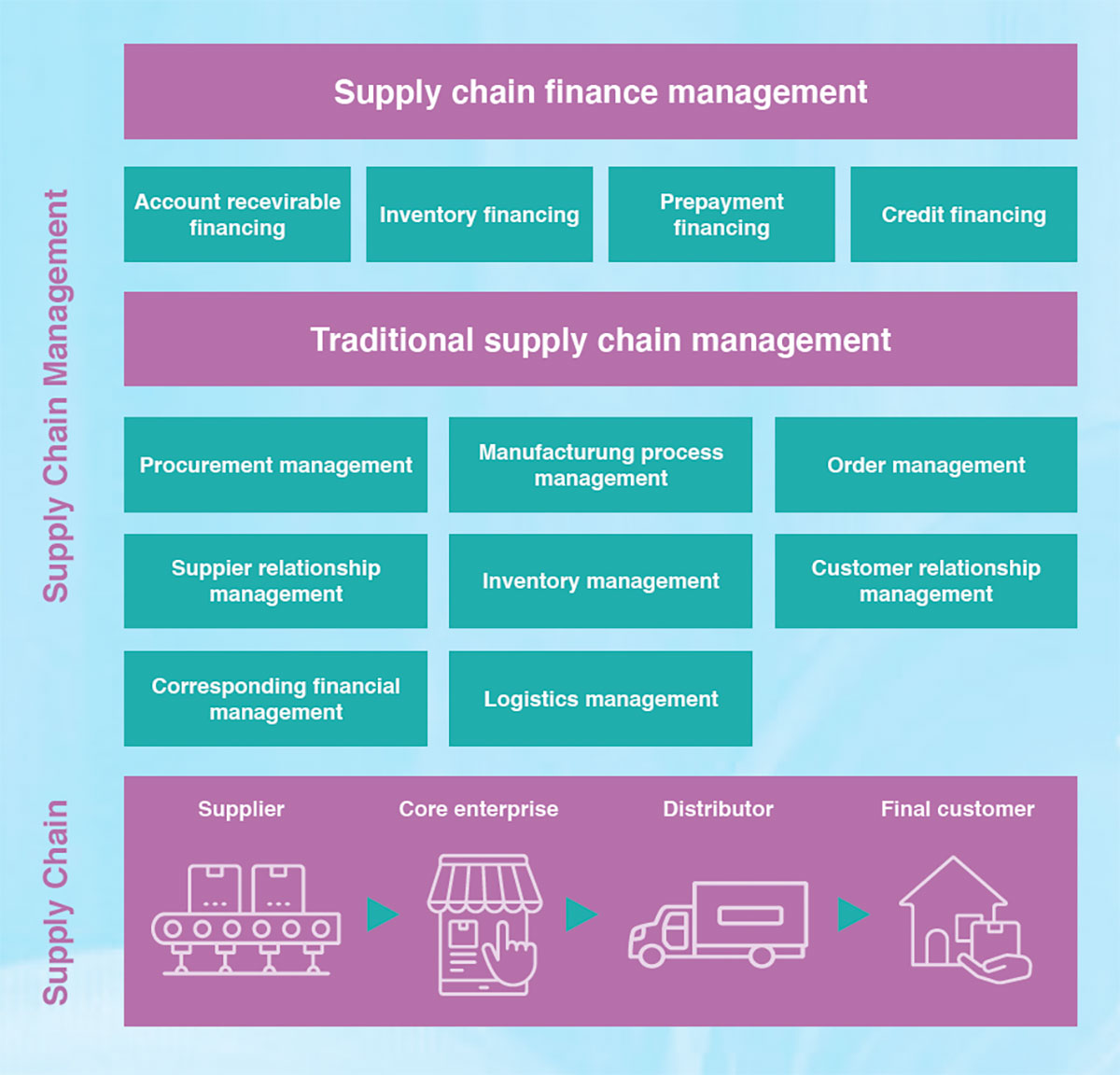

The promising role of supply

chain finance

Supply chain finance,

with its rich alternative

structured data, can be a

promising domain for AI

for loan issuing and risk

management.

To this end, we wish to suggest

that supply chain finance can be

a promising domain for AI and

machine learning applications: it

has rich alternative structured data,

which banks have not made use

of, or have no access to, for loan

issuing and risk management. A

supply chain is a network formed

by manufacturers, suppliers, and

distributors. The network has three

flows: flows of physical goods,

flows of information about the

goods, and flows of payments

of the goods and services. It

involves processes such as resource

integration, goods design and

manufacturing, procurement and

production, logistics, and sales

and services. Supply chain finance

involves financing and financial

management for supporting the

above-mentioned supply chain

processes. Typical supply chain

finance models include account

receivable financing, inventory

financing, prepayment financing,

and credit financing. The following

diagram represents the relationships

of supply chain, supply chain

management, and supply chain

finance.

Leveraging on the traditional loan indicators, such as ratio of loans to

total assets of the borrower, current

ratio, leverage ratio, liquidity

ratio and profit ratio, and on

continuously improved credit risk

assessments resulting from accurate

models, FinTech applications

in supply chain finance aim at

speeding up the credit scoring/

lending process and strengthening

risk management, including

liquidity management, business line

allocation, product line allocation,

and pricing.

Exploiting transaction data

Exploiting transaction data has

also becomes a key competitive

advantage in selling. Recently,

I started working with a new

IDBA student, Mr Lie Li. After

graduating from the UK, Mr Li

started a new business in crossborder

e-commerce. His business

turns out to be very successful. Mr

Li demonstrated to me examples of

how he exploits supply chain data in seeking best-selling products

on eBay and Amazon. Take the

eBay data for example, it not only

provides dynamic pricing and sales

data but also supplies website click

information such as "other items

customers have viewed."

Laboratory for Artificial

Intelligence Powered Financial

Technologies

In his recent budget speech, Hong

Kong Financial Secretary Paul

Chan indicated that the InnoHK

Research Cluster programme will

be officially announced in March,

an announcement that has been

delayed twice. When reporters

asked for details of the programme,

Secretary Chan declined to give

further advance information.

My friends asked me about my

opinions of the Financial Secretary's

speech on the InnoHK programme.

I told them to count only the

face value. "If you really want to

read between the lines," I added, "probably CE plans to make the

announcement, and he does not

want to steal the limelight from

his boss."Actually, CityU will host

three laboratories and Laboratory

for Artificial Intelligence Powered

Financial Technologies (AIFT) is one

of the three.

Rich alternative data

AIFT has identified

three R&D themes: AIdriven

financial services,

AI-enhanced financial

technology, and social

media analytics.

AIFT will work with City University

and Columbia University to

assemble a team of professors

and research students to conduct

academic research, train local

talents, and form start-up/spinoff

companies. AIFT has identified

three R&D themes: AI-driven

financial services, AI-enhanced

financial technology, and social

media analytics. Among them,

supply chain financing is one of

the intended projects. We plan to

extract business value from data,

and to develop the augmented intelligence to facilitate credit and

risk management decision-making.

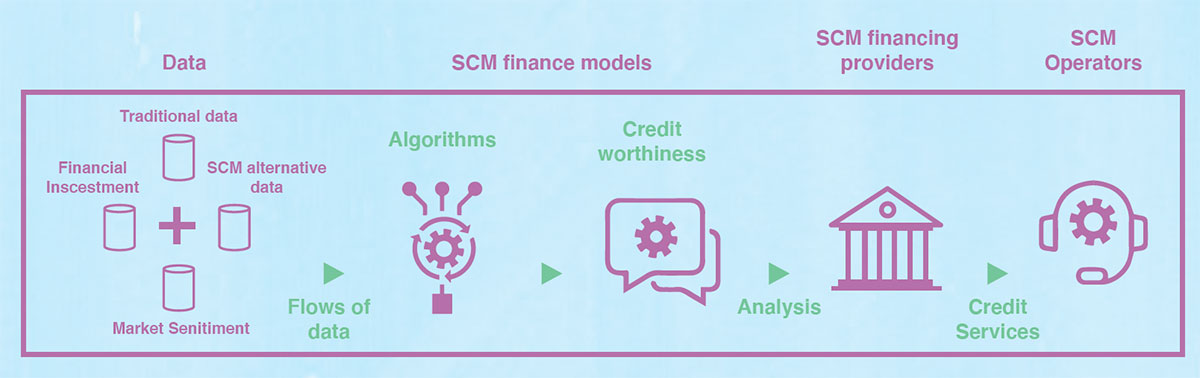

We have developed a conceptual

framework as follows.

Accounting and financial

information provide the traditional

data. Supply chain information

and market sentiment belong to

rich alternative data. Because of

the multi-party nature of supply

networks, we propose a federated

learning environment empowered

by gradient boosting decisiontrees.

In addition to traditional and

accounting-based loan indicators,

we plan to make use of modern

portfolio management and asset

pricing theories to evaluate credit

worthiness.

Novel research results at CityU

Novel research results at CityU

also shed new light into exploiting

supply chain alternative data and

developing machine learning

algorithms. For example, Dr

Junming Liu of the Department

of Information systems conducts

research work in an attempt to

find best-selling products. He has

developed a GCN-LSTM Deep

Ranking model that leverages

social media activities and their implicit influences on product

popularity. This information can be

used, in conjunction with supply

chain transaction information, as a

leading indicator for future sales. Dr

Yining Dong of the School of Data

Science is working on algorithms

to overcome the notorious lack of

interpretability of machine learning

algorithms by adopting gradient

boosting decision-tree to federated

learning. We are quite confident

that AIFT will provide useful results

and we welcome faculty, students,

and alumni to join in our efforts.

Professor Houmin Yan

Chair Professor

Department of Management Sciences