Dr Gavin Feng is an Assistant Professor of Business Statistics at the Department of Management

Sciences. In this article, Feng focuses on the interdisciplinary research between deep learning and asset

pricing factor investing. The particular innovation is understanding the discovery and construction of asset

pricing factors with a bottom-up deep learning model. This article is based on his co-authored paper

"Deep learning in characteristics-sorted factor models" with Nicholas Polson and Jianeng Xu from the

University of Chicago.

Models for stock returns

include Nobel Prize

research such as the Capital

Asset Pricing Model and

the Fama-French 3-factor

model.

Asset pricing models study why

different assets attract different

expected returns. Examples of such

models for stock returns include

Nobel Prize research such as the CAPM (Capital Asset Pricing Model)

and the Fama-French 3-factor

model. In 2020, we present a

bottom-up approach based on deep

learning applied to the construction

of asset pricing models, which

include firm characteristics (inputs),

risk factors (intermediate features),

and security returns (outputs). The

question addressed using deep

learning, one special method

in machine learning, is how to

improve asset pricing models to

explain the cross-sectional average

returns.

According to ICAPM of Merton

(1973), a combination of common

tradable factors captures the crosssection

of expected returns, and the

regression intercept should be zero.

Ri,t = αi + β1,i ∗ 1,t + · · · + βk,i ∗ fk,t

+ Ei,t

Therefore, the model fitness for asset

pricing is not about the explained variation in time series, but the

magnitude of intercepts, alphas, in

the cross-section. This non-arbitrage

restriction on alphas implies that

simply adding factors leads to

statistical overfitting (time series

R2) but does not cause economic

overfitting (intercepts).

Researchers typically

sort securities on firm

characteristics and create

long-short portfolios as

common risk factors to

build asset pricing models.

In empirical studies, researchers

typically sort securities on firm

characteristics and create long-short

portfolios as common risk factors to

build asset pricing models. The goal

is to explain the time-series variation

of multiple asset returns and their

average returns' cross-sectional

variation. For example, Fama and French (1993) add SMB (small-minusbig)

and HML (high-minus-low) to

CAPM. However, in the asset pricing

literature, almost all proposed factor

models have rejected the zeroalpha

hypothesis. Therefore, we

want to approach this puzzle, with a

machine learning perspective, as an

optimisation problem: How does one

construct a factor model to minimise

pricing errors or alphas?

How does one construct a

factor model to minimise

pricing errors or alphas?

The goal of their paper is to

investigate the underlying

mechanism of the characteristicssorted

factor models, which includes

sorting securities, generating

factors, and fitting the cross section

of security returns. The particular

focus is the cross-sectional variation

of asset average returns. They

define an non-arbitrage objective

function, pricing errors, for the

optimization problem. They show

the characteristics-sorted factor

models can be dissembled as a deep

learning architecture (see Figure

above).

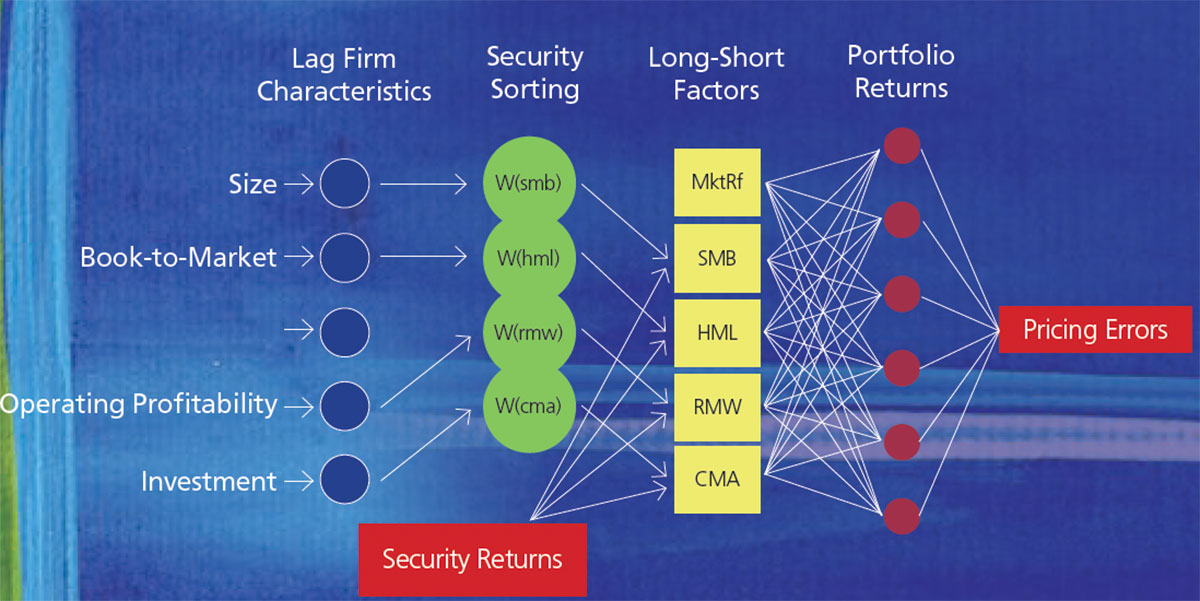

This figure provides a deep learning

representation of building the

Fama-French 5-factor model using

firm characteristics to calculate

the objective function, pricing

errors, for portfolio returns. The lag

characteristics are inputs. The longshort

factors are hidden neurons. The

portfolio returns are outputs.

(1) Inputs are firm characteristics. The neural network starts from sorting securities on firm characteristics, which is a non-linear activation to create long-short portfolio weights.

(2) Intermediate features are risk factors. The factors are linear activations (long-short portfolio weights) on realised returns from the sorting directions.

(3) Outputs are security returns. Minimising an economic objective function is equivalent to minimising pricing errors for fitting the factor model to portfolio or individual stock returns.

The focus is on "training

a factor model" rather

than "testing a factor or

characteristic."

Distinct from the literature on

stochastic discount factors, we

focus on training a factor model

rather than testing a factor or

characteristic. Apart from the PCA literature, their innovation is to

apply dimension reduction on firm

characteristics (inputs) rather than

the characteristics-sorted factors

(intermediate features). We argue

the current literature is mostly about

intermediate features and outputs

(security returns), whereas ours

illustrates the complete channel

between inputs and outputs. We

adopt a non-reduced-form neural

network and develop such a bottomup

approach that includes security

sorting, factor generation, and fitting

the cross-section of security returns.

The Fama-French-type characteristicssorted

factor models can be shown

as "shallow" learning models.

Dr Gavin Feng

Assistant Professor

Department of Management Sciences