A bubble? A fraud? A way to the future? A currency? Digital gold? With all the recent fuss about bitcoin, its identity seems as mystic as its creator, Satoshi Nakamoto. The good news is that, unlike Satoshi, who intentionally tries to remain anonymous, bitcoin was designed to be transparent from day one, at least to those who are willing to dig into its open source programme files.

This article is meant to be a non-technical introduction to provide the big picture of bitcoin. So please allow me to leave most of the computer science, game theory, and cryptography details under the hood. For those who want to understand bitcoin’s inner-workings, Bitcoin and Cryptocurrency Technologies: A Comprehensive Introduction, published by Princeton University is a great read.

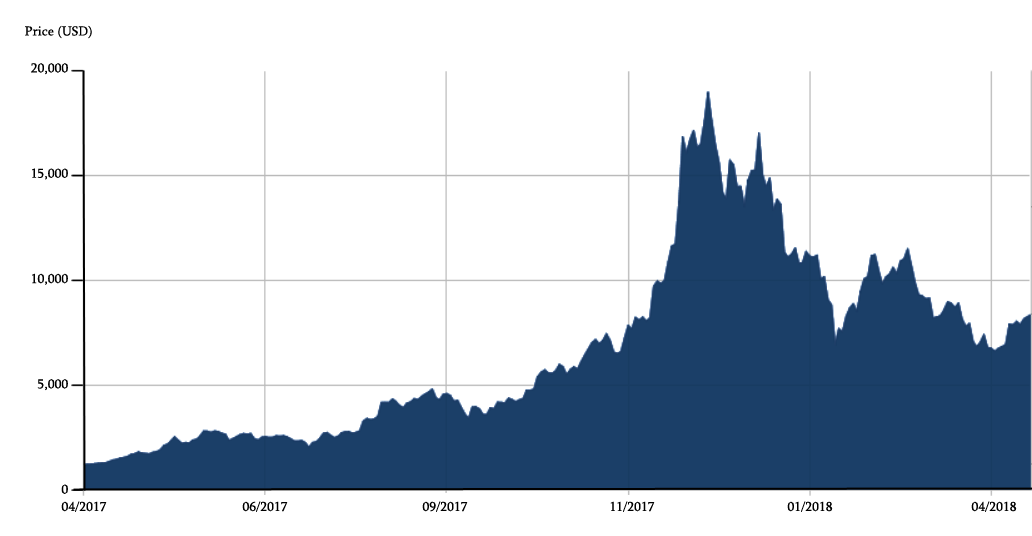

Tumultuous Price Change of Bitcoin 2017-2018

Two pizzas = 10,000 bitcoins

Bitcoin is the result of a decade-long quest to create a decentralized alternative to government controlled, centralized monetary systems. It was not technically possible until we reached the mass adoption of the internet and developed the idea of open-source software. Bitcoin was launched on 9th January 2009, after the publication of Satoshi Nakamoto’s white paper “Bitcoin: A Peer-to-Peer Electronic Cash System”. For over a year, bitcoin remained a “garage project” for Satoshi and a few of his cyberpunk followers, without any actual interaction with the “real world”. But on 22nd May 2010, Laszlo Hanyecz, a bitcoin software developer, bought two Papa John’s pizzas with 10,000 bitcoins, thus creating the first record of bitcoin price in US Dollar terms. It is incredible to compare bitcoin’s humble beginnings with its current over US$100 billion market capitalization.

How does it work?

Bitcoin is the “token” of its decentralized blockchain system, which creates a public consensus about the supply, ownership, and transaction of bitcoins. In other words, bitcoin’s internet based blockchain is the platform of an alternative monetary system, meant to be control-free from any entity. Bitcoin as a token and its blockchain complement each other to make this ecosystem work (or not work), so we must always evaluate them together, not separately. Arguing that blockchain is good but bitcoin is bad, or vice versa, is equivalent to arguing car is good but gasoline is bad. All educated people should avoid that.

Why does this system need a token at all? Because it is decentralized without central control. All the rules are coded within bitcoin’s software protocol. If you don’t like it and change the protocol, the stuff you run is no longer a bitcoin system, and other bitcoin users will not recognize your coins. To make sure all the players, especially the “miners” who contribute computing power and extend the blockchain, behave in the interests of the system, there are two incentivizing mechanisms, one positive, one negative, and both of them rely on the value of bitcoin.

Mining rewards

The positive incentive is a “mining” reward in the form of bitcoins. The first (and only the first) successful miner who collects newly validated transactions, and solves the built-in computational puzzle to create the next block of transaction data, will be rewarded in bitcoins. This reward includes both newly “minted” bitcoins according to the supply rule in the protocol, and existing bitcoins paid by users as an optional transaction fee. As the total supply of bitcoin is capped at twenty-one million and, as estimated, this cap will be reached by around 2140, the optional transaction fee will become the majority of mining reward. As of March 2018, close to seventeen million bitcoins have already been mined, meaning that there are only four million more bitcoins left to be created in the future. To the miners, if they behave neutrally, they can expect a highly predictable share of mining reward that is proportional to their share of all contributed computing power in the system. For example, if you control 10% computing power, measured by hashrate, of the entire bitcoin network, then your chance of being the winner of each block is simply 10%.

The negative incentive is the “mining” cost in solving the computational puzzle. It serves as a punishment for manipulating the system. In bitcoin’s blockchain, if you want to mess with the current consensus, for example to spend the same bitcoin twice (double-spending attack), your chance of success is directly tied to your share of overall computing power. If you only control a small fraction of the system’s computing power, your chance will be so low that it won’t be worth doing so. Your chances improve significantly when you control close to fifty percent of all computing power. But that means you have already deeply invested in bitcoin mining and can receive close to half of all mining reward in bitcoins. So it doesn’t make sense to harm the system’s credibility as a major stakeholder and make your bitcoin reward worth less or zero.

Of the people, by the people, for the people

When the bitcoin system is up and running 24/7, as it is now, it serves as an internet based, decentralized monetary system that does not belong to and is not controlled by any government, central bank, or private entity. Many commentators believe this is a lethal weakness. But in fact, this is exactly what bitcoin was created for, a monetary system “of the people, by the people, for the people”. Nobel laureate and Austrian School economist Friedrich Hayek published The Denationalization of Money in 1976, and advocated a decentralized monetary system similar to cryptocurrency, but it was technically very different due to the absence of an internet.

Whether bitcoin’s system will succeed, and how much each bitcoin will be worth, all depends on the public’s confidence in the decentralized system’s credibility, compared to the national fiat monetary system or other cryptocurrencies’ systems. In countries with less credible monetary policy, e.g. Venezuela, bitcoin has already gained popularity as a medium of exchange. How much we can trust bitcoin depends on the quality of its blockchain consensus, which in turn depends on miners contributing plenty of computing power in an honest fashion. In the end result, a valuable bitcoin is the only way to properly incentivize miners in this decentralized system. So now we close the loop of bitcoin’s value analysis.

A system of distributed trust

Can someone destroy bitcoin’s system? Yes, but it would be extremely difficult. Decentralized blockchains work like “Skynet” in the Terminator movie. It is distributed across the entire internet, and has no central server or “kill switch” whatsoever. To destroy bitcoin, one must locate and wipe out each and every copy of its blockchain information from all data storages in this world, both online and offline. Because even if only one complete copy survives the attack, the blockchain can replicate and spread into countless connected computers again.

Can governments ban bitcoin? Yes, but they must completely censor the internet. It is in fact not banning bitcoin in a country, but rather blocking that country from accessing bitcoin related internet content. I doubt any truly developed society would do that. In fact, Germany just passed a law that regards bitcoin as the equivalent to legal tender for tax purposes if used as a means of payment.

Can central banks create their own cryptocurrencies to substitute bitcoin? Clearly not, because blockchain controlled by a central bank is by no means decentralized, and still requires the public’s trust in one entity. In fact, a centralized blockchain does not need a valuable token or the computational puzzle to incentivize the miners, as the only miner is the central bank itself. Therefore, a central bank cryptocurrency would simply need government credibility to work, just as fiat money does nowadays.

Tulip Bubble 2.0?

Is bitcoin a Tulip Bubble 2.0? If we multiply its current price and supply, bitcoin’s total market value is around US$180 billion at the time of writing. Coca-Cola has a higher market capitalization than that. Bitcoin is certainly facing a lot of challenges, both technical and political. But to anyone with a solid grasp of its underlying blockchain technology and its potential to serve as a borderless, control-free medium of exchange and store of value for any person who can access the internet, bitcoin valued at around the market capitalization of a food and beverage company looks like a steal.

Bitcoin mining consumes roughly as much energy as the Republic of Ireland